You are here

Back to topFollowing its issuance of Regulation No. 10/POJK.05/2022 (the P2P Regulation) and 2023-2028 roadmap for the peer-to-peer (P2P) lending sector, Indonesia’s Financial Services Authority (OJK) has now issued Circular Letter No.19/SEOJK.06/2023 on Implementation of Information Technology Based (Peer-to-Peer) Lending Services (the P2P Circular Letter).

Developments in Indonesia’s P2P market leading up to issuance of P2P Circular Letter

The P2P Circular Letter introduces more stringent requirements against a backdrop of the increasing volume of P2P loans and reports of declining performance in the sector. Based on the figures available on its website (www.ojk.go.id), OJK recorded a year-on-year increase in online lending of 28.11 percent in May 2023, with loans totalling Rp.51.46 trillion (about US$3.32 billion).

While OJK reported a TWP90 of 3.36 percent (the percentage of loan defaults and non-performing loans exceeding 90 days) in May 2023 (still well below the threshold of 5 percent), news reports suggested that several peer-to-peer lending platforms (P2P platforms) ended the year with a TWP90 exceeding 5 percent. There were also reports of unfair business practices by several P2P platforms, mainly due to lack of transparency. These developments likely informed OJK’s decision to tighten the requirements for this sector by issuing the P2P Circular Letter.

Key changes

The P2P Circular Letter regulates various technical aspects, including funding distribution and repayment mechanisms, maximum economic benefit, risk management for users, data and information management, and debt collection. It also formalises several industry rules previously governed by the 2020 Indonesia Fintech Lending Association (AFPI) Code of Conduct.

One significant change is a new limit on maximum economic benefit. Previously, interest rates and penalties had been left to AFPI to regulate under its Code of Conduct. This practice attracted the attention of the Indonesian Competition Commission (KPPU), which commenced an investigation of potential breaches of Indonesia’s Competition Law in October 2023. OJK’s decision to regulate economic benefit in the P2P Circular Letter has provided greater certainty for the P2P lending sector.

While the P2P Circular Letter took effect on 8 November 2023, P2P platforms are given time to comply with some of its provisions. Funding agreements signed before the issuance of the P2P Circular Letter will continue to be valid, but amendments must comply with its newly introduced requirements.

Borrowers’ eligibility, distribution and repayment

The P2P Circular Letter contains further details on how the P2P lending business should be carried out, including on fund distribution and repayment mechanisms.

First, the P2P platform must display certain prescribed information relating to itself and its products, such as reminding lenders that all risks associated with the funding (unless caused by the P2P platform’s negligence or mistakes) are borne by the lenders, and must ensure that prospective customers understand that before they register.

Post-registration, the P2P platform and its users must take certain steps for the loan applications and fund disbursements. For instance, the P2P platform must assess funding eligibility of each loan applicant, including, among other things, the applicant’s capacity to repay (specifically for consumptive loans), whether the applicant has obtained loans from other P2P platforms, and their economic prospects.

A prospective borrower’s capacity to repay a consumptive loan is measured by comparing the ratio of the loan principal and economic benefit with the borrower’s income. The maximum ratio for this is currently set at 50 percent, and this will be gradually lowered to 30 percent over three years.

Notably, the P2P Circular Letter prohibits P2P platforms from outsourcing either the assessment of funding eligibility or their information technology (IT) function.

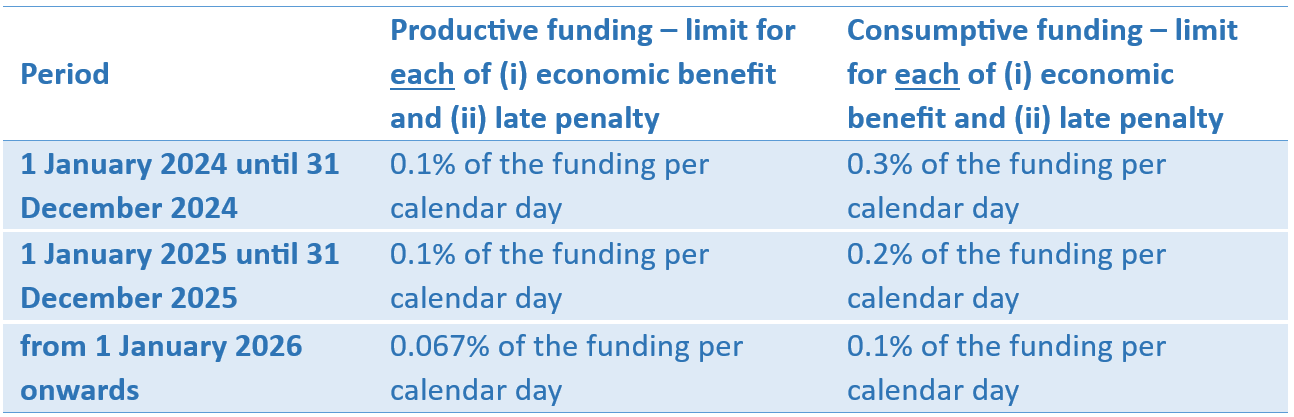

Maximum economic benefit

The “maximum economic benefit” concept in Article 29 of the P2P Regulation is clarified in the P2P Circular Letter as return rates (tingkat imbal hasil), which include: (i) interest/margin/profit sharing; (ii) administrative fees/commissions/platform fees (ujrah); and (iii) other fees aside from late payment penalties, stamp duty or taxes.

Imposing limits on the overall economic benefits received by P2P platforms ensures that borrowers are protected from the hidden fees that some P2P platforms have imposed in the past.

In 2020, AFPI set maximum daily (i) interest and other fees and (ii) late penalties at 0.8 percent each of the total loan amount. So, a borrower failing to pay on time could face total interest and late penalty fees of 1.6 percent per day, subject to an overall cap equal to the loan principal. These numbers were lowered in October 2021, when the total interest, loan, and other fees (other than late penalties) were set at a maximum of 0.4 percent daily, again subject to an overall cap equal to the loan principal.

The P2P Circular Letter lowers these limits as set out in the table.

The P2P Circular Letter also includes the same overall cap for these charges of 100 percent of the funding amount under the financing agreement. Note that OJK has the discretion to re-evaluate these thresholds by considering economic conditions and industry developments.

Mitigation of risks for users

P2P platforms are expected to undertake a range of measures to mitigate risks for their users, at least including:

- risk analysis on the loan being applied for;

- verification of user identity and authenticity of documentation;

- carrying out debt collection on loans disbursed in an optimal manner;

- facilitating transfer of funding risks, for instance, through insurance and/or loan guarantee mechanisms; and

- facilitating transfer of risk over collateral objects by, for example, insuring the collateral or cooperating with third parties to store the collateral.

In undertaking risk assessment and verification of user identity mentioned in points (a) and (b), P2P platforms may use data from various sources while ensuring compliance with personal data protection regulations.

Data and information management

The P2P Circular Letter includes requirements concerning the management of data and information collected from user devices.

P2P platforms must maintain the confidentiality, security, integrity, and accessibility of the personal data and information, transaction data, and financial data that they manage, from when the data and information are received until they are destroyed.

P2P platform access to user devices is limited to camera, location and microphone. (There have been concerns that some P2P platforms go beyond this and have accessed the data stored on user devices for debt collection purposes.)

Without properly documented written approval from users (aside from regulatory exclusions), P2P platforms must not share user data and information with any other parties. Where data transfer has been approved by the user, the P2P platform must ensure the recipient only uses the data for the agreed purpose.

Debt collection and emergency contact use

The P2P Circular Letter reiterates the P2P Regulation requirement for P2P platforms to deliver a warning letter (setting out the prescribed minimum information) after the lapse of the relevant funding period and the due date. Prior to the repayment due date, P2P platforms must send periodic reminders to borrowers.

A P2P platform may collect debts independently or by engaging third party debt collectors, but shall bear full responsibility for the debt collection process. Debt collection may be done through desk collection (indirect collection including through short messages, phone or video calls, and other media) and field collection (ie, in-person collection). Whatever collection method is used, the P2P platform must ensure that debt collectors are properly trained and certified, and must follow the ethical guidelines in the P2P Circular Letter.

The P2P Circular Letter reconfirms that emergency contact details may only be used to locate the borrower and not to seek repayment directly from the emergency contacts. The P2P platform must clarify with and seek confirmation and approval from the owner of the emergency contact data before using their details.

Publication of funding performance

Funding performance must be published by P2P platforms on their websites, applications, and/or electronic systems. Notably, P2P platforms are expected to display the most up-to-date weekly information on repayment success rates (Tingkat Keberhasilan Bayar or TKB) on the top right of the main screen, where it is easy to be seen and read. The information shown must include TKB0 (repayment on due date), TKB30 (repayment within 30 calendar days from due date), TKB60 (repayment within 60 calendar days), and TKB90 (repayment within 90 calendar days).

Sanctions

Breaches of certain requirements under the P2P Circular Letter may lead to the administrative sanctions set out in the P2P Regulation, which include a warning letter and restriction of business activities.

Key Takeaways

The increased use of P2P platforms in Indonesia raised the urgency to create a more sophisticated regulatory framework. The P2P Circular Letter will have an impact on the day-to-day operation of P2P platforms, including a potential negative impact on P2P platform revenues in the short term. However, the increased protection for borrowers and the overall strengthening of the regulatory framework may encourage more people to use P2P platforms, which in turn should encourage more sustainable medium- and long-term growth in this sector.

We are continuing to monitor developments in the P2P lending sector and expect OJK to issue further regulations and guidance in the year ahead.